What Is Saylor Really Doing?

The math behind the infinite money glitch

There is a lot of talk about MSTR 0.00%↑ these days, but do you really understand what Michael Saylor is doing, and what the risks of his layered capital structure are?

I didn’t, so I dove to the very bottom.

You may not like Saylor, you may even not like Bitcoin, but from a pure math perspective Strategy is pretty damn interesting. Let’s explore how the “money glitch” works so moving forward you can understand the numbers and enjoy the show fully while it’s unfolding.

How it started.

In 2020, at the beginning of COVID, like most of the market, the MicroStrategy stock tanked badly. It was a follow-up to many years of declining price and revenue. Saylor had a problem.

When central banks fired up the money printers in response to COVID, the U.S. money supply exploded by 26% in a single year (compared to the usual 5–6% annual growth). With near-zero interest rates, Saylor calculated his cash was generating real yields of –15% to –26%. He famously called it “toxic,” “trash,” and a “melting ice cube.”

Ironically, Saylor had been a skeptic who’d tweeted in 2013 that Bitcoin would “go the way of online gambling.” But in 2020, facing the unprecedented monetary expansion, and after looking into different options, he finally got his Bitcoin epiphany: fixed 21-million supply made it superior digital gold—a true store of value in an era of infinite money printing.

It’s Bitcoin. They need to buy Bitcoin.

In August 2020, MicroStrategy made its first purchase: $250 million for 21,454 BTC.

The Glitch

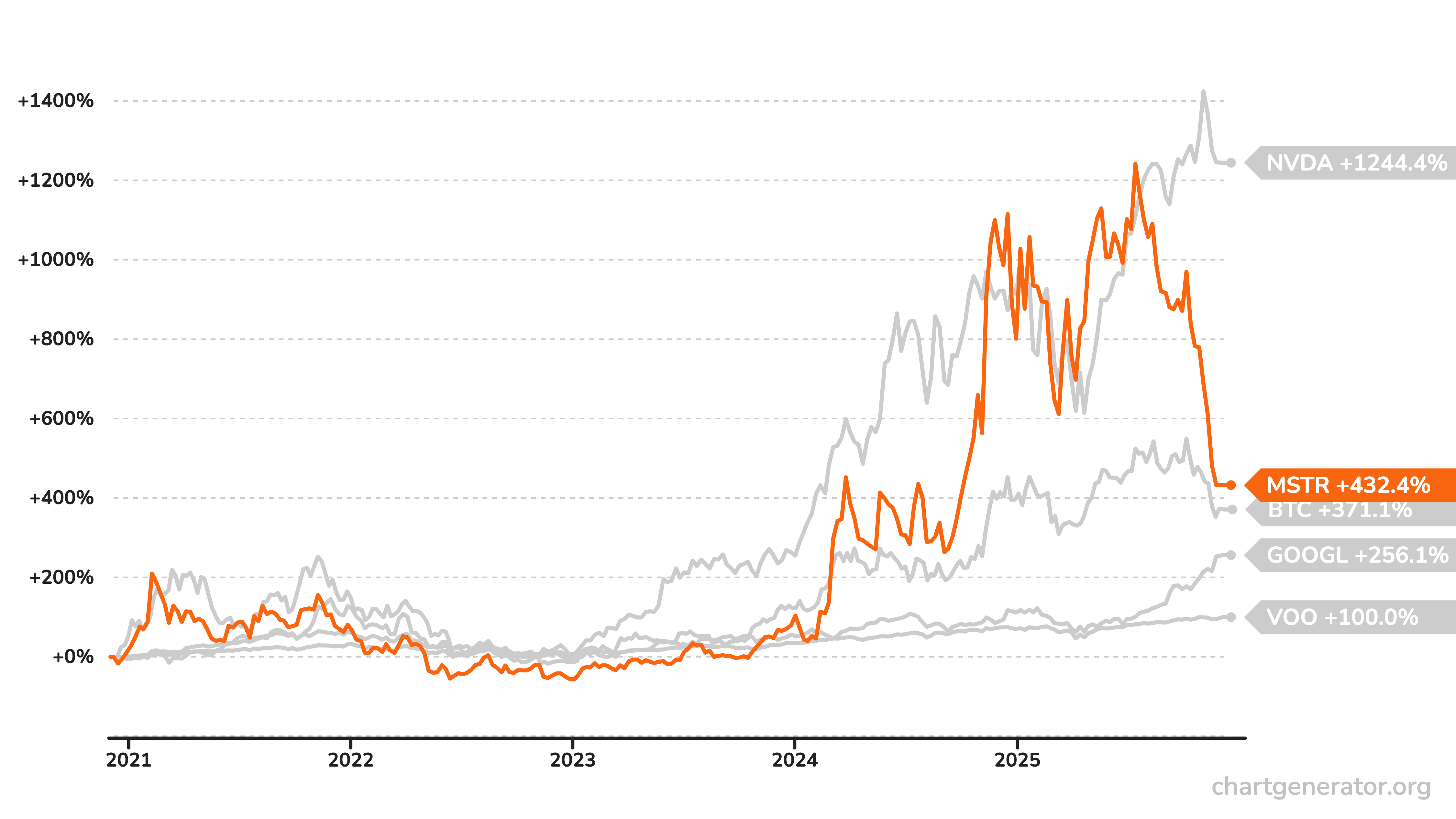

The market responded enthusiastically, and the stock reached the highest level in over 20 years. At the time, there were no Bitcoin ETFs, so MSTR 0.00%↑ offered convenient Bitcoin exposure for stock investors around the world.

In fact, the stock started trading at significant mNAV premium (modified Net Asset Value) meaning, the market cap of the company was significantly higher than the value of Bitcoins on the balance sheet. Here is where the “money glitch” discovery happened:

Imagine that Microstrategy has Bitcoin worth $1M, but the market cap of $2M. This means the mNAV of 2.0. If they issue additional $2M of stocks and buy Bitcoin, now the holdings are worth $3M, while the market cap is $4M, the mNAV goes down from 2.0 to 1.33.

Yes, the premium allows them to print money and buy more Bitcoin—debt free, at least initially.

That’s the beginning of the magic math. That’s the glitch.

Matt Levine summarized it ironically:

The basic idea is that the US stock market will pay $2 for $1 worth of crypto.

But why?

You may ask: why would anybody do that? Great question. The answer is: leverage.

Since the stock is not pegged to Bitcoin like an ETF, the mNAV goes up and down, offering traders leveraged exposure to Bitcoin without margin calls or the cost of servicing debt.

Leverage without margin call is the product.

You may roll your eyes, but there are many Bitcoin traders that like the leverage, and MSTR 0.00%↑ is a volatile stock that offers it. However, this mechanism had its limits:

In 2020-2023, many institutional investors (pension funds, certain ETFs, retirement accounts) literally couldn’t buy Bitcoin directly. MSTR 0.00%↑ was the only way in. This structural demand helped sustain the premium. The January 2024 spot ETF approvals changed it—suddenly BlackRock offered the same exposure at 0.12% fees. That’s partly why mNAV compressed from 3.4x to 1.15x.

Saylor was too good at math to stop there. With Bitcoin’s massive average annual growth, and the company still having some revenue from the legacy business, he saw an even bigger opportunity.

If Bitcoin appreciates faster than the cost of debt, why not borrow money to buy more? This is where it gets both interesting and complex at the same time.

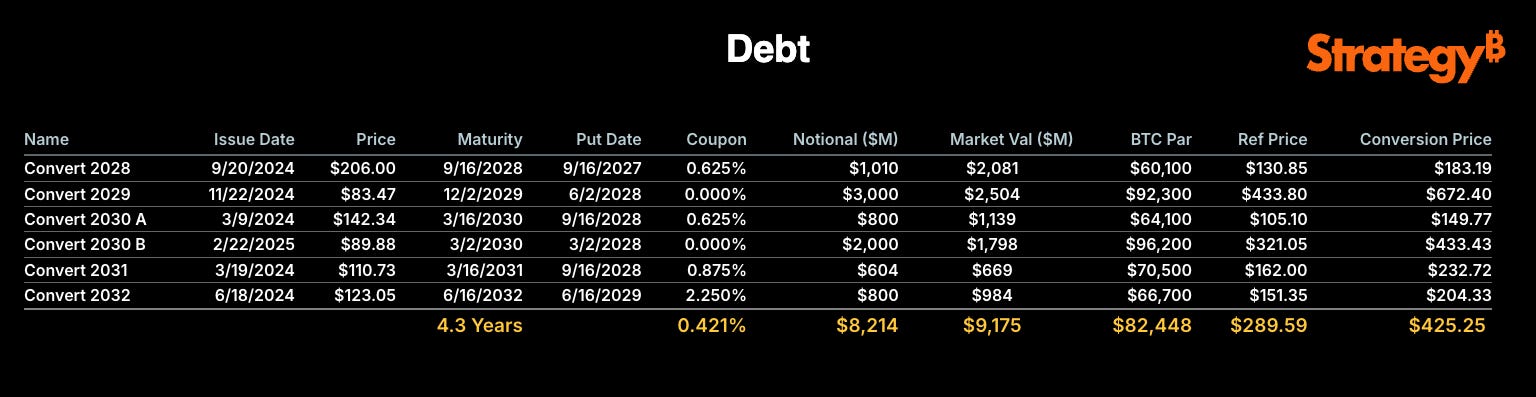

Convertible Bonds

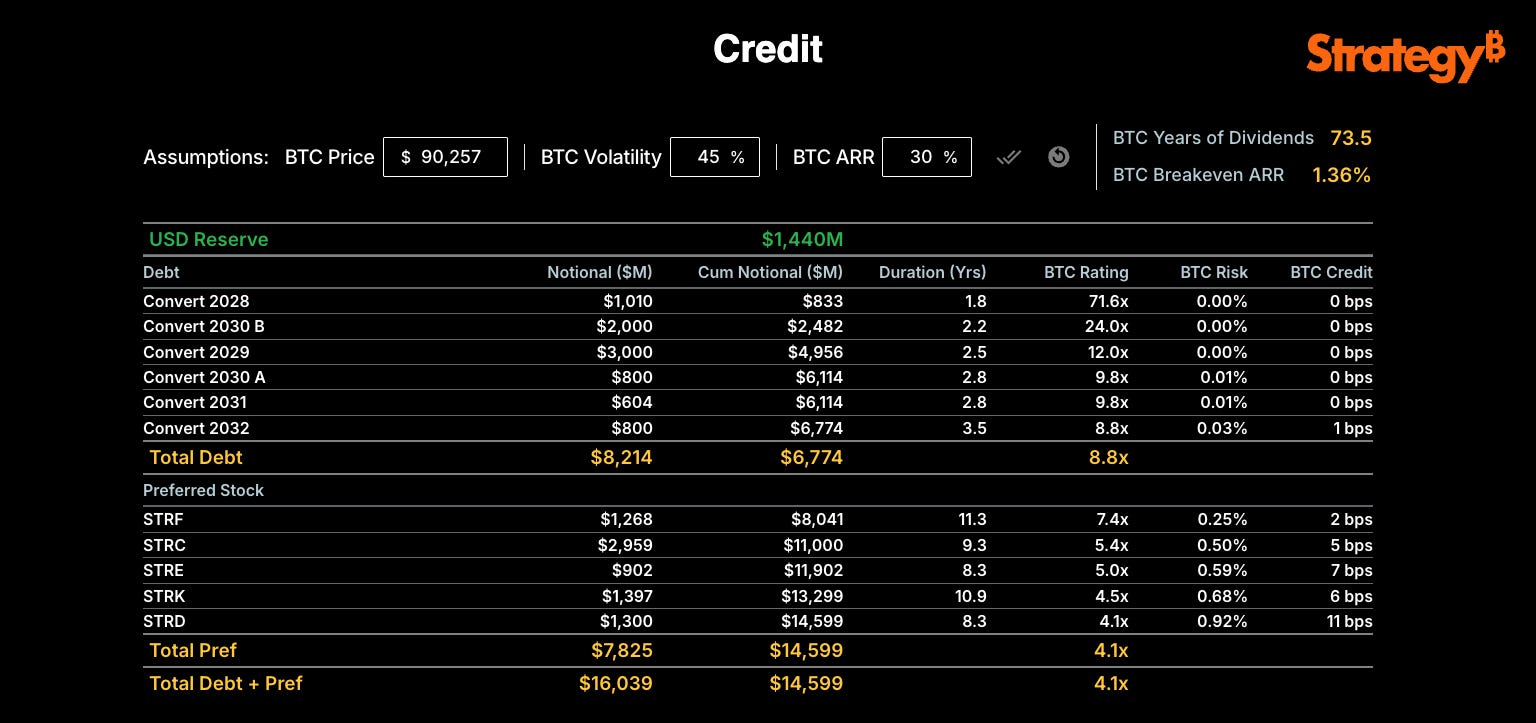

Between 2020-2025, Strategy issued $8.2 billion in convertible bonds—part loans, part stock options. Here is how they work:

Normal bond: You lend a company $1,000. They pay you interest (say 5% annually) and return your $1,000 at maturity. Simple.

Convertible bond: You lend a company $1,000. They pay you lower interest (say 0.5%), BUT you get the option to convert your bond into stock at a predetermined price. If the stock moons, you convert and profit. If it doesn’t, you still get your $1,000 back.

Now, let’s look at the terms:

The average coupon is merely 0.42%—essentially free money to buy an asset that historically compounds at 50%+ annually.

Two of the bonds (Convert 2029 and Convert 2030 B) pay literally zero interest. It may seem confusing why anyone would lend at 0%, until you realize the potential profit at conversion is +55% and +74%.

Bondholders have legal claims.

If Strategy can’t repay at maturity, bondholders can force company to liquidate the Bitcoin. The conversion feature helps—if MSTR is above the conversion price, bondholders happily convert to equity instead of demanding cash.

The risk starts to be visible only when the stock price falls:

Convert 2028 has a $183 conversion price, roughly the current price, so it’s at the money, but if MSTR 0.00%↑ drops to $150 by the September 2027 put date, those bondholders won’t want underwater stock. They’ll demand their $1 billion in cash.

How it’s going.

When mNAV compressed, equity and debt issuance slowed down. At the beginning of 2025, around the time the company removed “micro” from the name and rebranded to Strategy, they also pivoted to preferred stocks—a hybrid between bond and stock.

The “Accretive” Problem

Let’s get back to the “infinite money glitch” math example first:

If the number of shares doubles, but Bitcoin holdings triple, it increases “Bitcoins per share”—which Strategy emphasizes, calling it “accretive”—but they’re quiet about stock dilution: current shareholders own less of the company due to the permanently increased total number of shares.

Convertible bonds have another issue: they allow hedge funds to profit risk-free from MSTR’s volatility while extracting value from common shareholders:

When Strategy issues a 0% convertible bond, hedge funds buy the bond and simultaneously short MSTR stock.

If MSTR rises, they convert the bond to shares at the preset price and cover their short—capturing the spread.

If MSTR falls, they profit on the short position while still holding a bond that gets repaid at full value. Either way, the hedge fund wins.

The cost? Common shareholders get diluted when bonds convert to shares—precisely when the stock is high and dilution hurts most. Strategy emphasizes “we raised $8 billion at 0% interest!”—but stays quiet about how convertible arbitrage extracts value from volatility that rightfully belongs to equity holders.

That’s where “preferreds” come to the rescue:

Preferred Stocks

While common stock gives you a piece of the company, preferred stock gives you a “senior” claim with fixed dividend payments (like bond interest), but limited upside.

Seniority means that if the company goes bankrupt, preferred holders get paid before common shareholders but after bondholders.

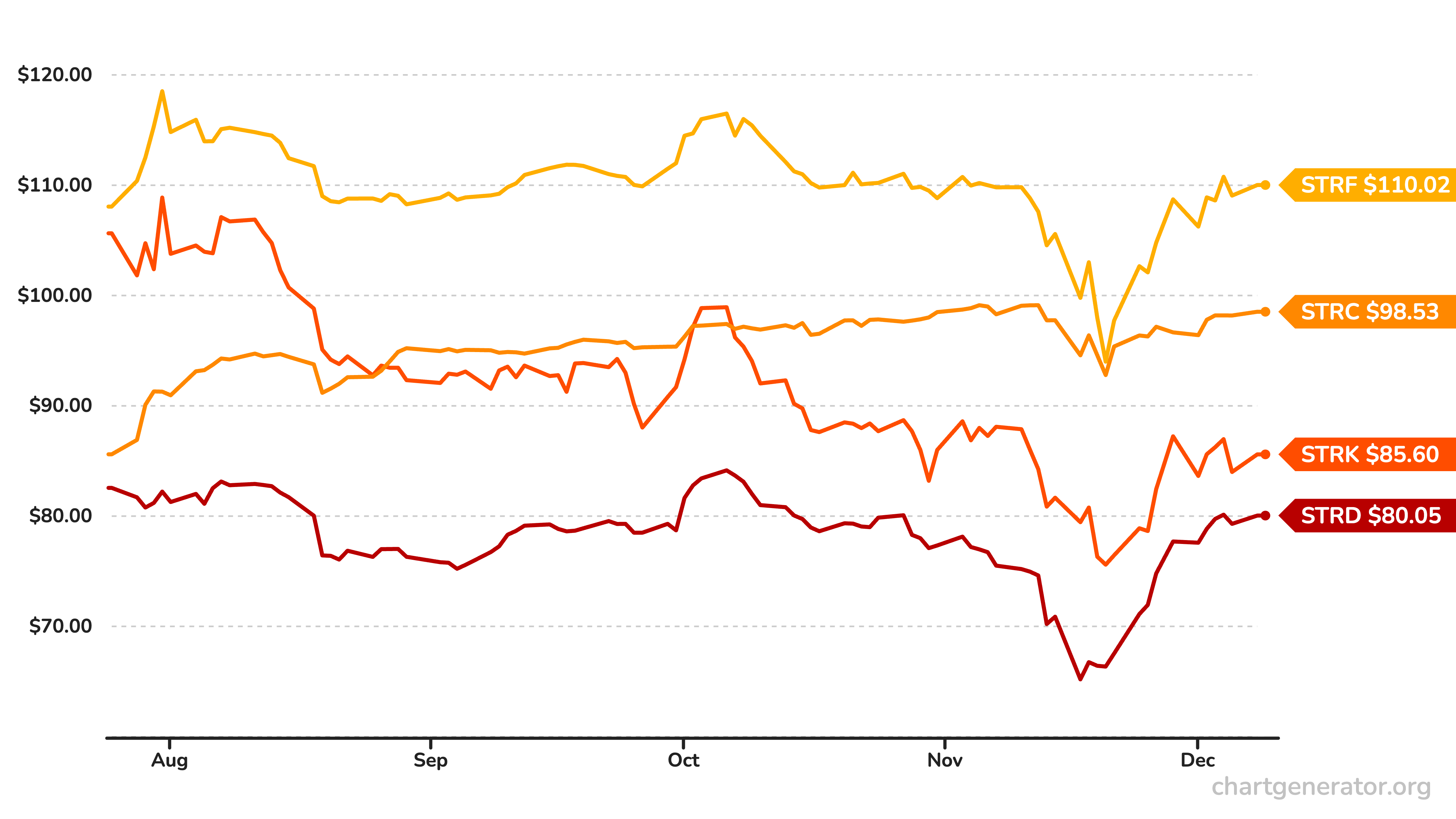

Preferred stocks are right in the middle: like bonds, they offer yield, but unlike bonds, they have no maturity date, no common stock dilution, and dividends payment flexibility. Strategy issued five classes of them, each with different seniority and terms:

Highest Seniority

STRF 0.00%↑ (Strife): 10% cumulative dividend. Payments can be skipped, but they compound at 11-18% until paid. Most protective—designed for pension funds seeking stability.

STRC 0.00%↑ (Stretch): Variable rate (~10.75%) compounding monthly dividend. Payments can also be delayed, but there is no “yield penalty” for it.

Middle Seniority

STRK 0.00%↑ (Strike): 8% cumulative with conversion option—each share converts to 0.1 MSTR at $1,000. For investors wanting both yield and Bitcoin upside.

$STRE (Stream): Euro-denominated for the European market, 10% cumulative. It works similarly to Strife, but has lower seniority. This one is likely the least relevant for most readers since it’s only accessible to institutional investors.

Lowest Seniority

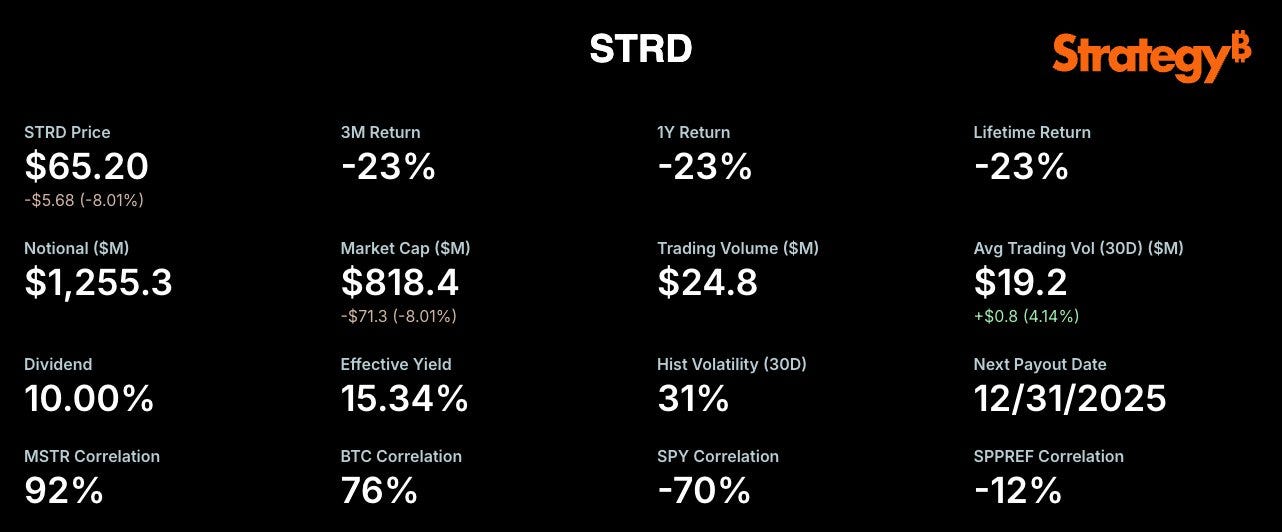

STRD 0.00%↑ (Stride): 10% non-cumulative—the key difference. If Strategy skips a dividend, it’s gone forever. Higher risk, but it trades at $80, giving a ~12.5% effective yield versus STRF’s ~9% at $110.

All preferred dividends are paid quarterly, except STRC, which pays monthly.

Preferred stocks aren’t unusual—Bank of America, Wells Fargo, and JPMorgan all have publicly traded preferreds yielding 5–7%. What’s unusual is Strategy offering 10% yields on stocks backed by Bitcoin.

A Few Months Later…

These preferreds have existed for less than a year, but we can already see how they behave under normal market conditions. In theory, they should all trade around $100, but as you can see, the market value them exactly by their seniority:

Premium or discount represents what investors think about probability of getting paid. The highest seniority STRF 0.00%↑ trades at 10% premium, while non-cumulative lowest seniority STRD 0.00%↑ dropped to $65 during a Bitcoin dip. That’s interesting because the yield is promised for the nominal price of $100, so the effective yield (if paid) goes up to 15%.

Now you almost understand preferreds:

Perpetual income. No maturity date. Collect 8-10% annually.

Indefinitely? Not quite:

Strategy can redeem them back at $100 per share.

Dividends aren’t guaranteed. We already discussed that part.

Inflation erodes the value of each share over time (something many miss).

Finally: the company could fail. We’ll talk about it later.

So, there is one big question to answer left.

Is It a Ponzi?

Let’s look at the actual numbers:

Strategy holds 660,624 BTC worth ~$59.5 billion at current prices. Total obligations (debt + preferred) are $16 billion. That’s a 4.1x coverage ratio—selling 24.4% of Bitcoin holdings would be enough to pay all the company debt back despite not having to be paid anytime soon.

The BTC Breakeven ARR of 1.36% means if Bitcoin appreciates just 1.36% annually, the holdings generate enough value to cover all obligations indefinitely.

Strategy appears absolutely safe… for now.

Paper Appreciation Doesn’t Pay Cash Dividends

Let’s imagine a problematic scenario:

The first convertible put date is September 2027 ($1 billion). If BTC is at $50K and mNAV is 0.6x by then, refinancing becomes very expensive or impossible.

Today, that sounds impossible, but a big part of the problem is that the plan is to continue issuing shares and debt, and in 2027, the numbers will be different, and hard to estimate now.

Strategy needs $811 million annually to pay preferred dividends. The legacy software business doesn’t cover even half of it, so where does the money come from?

Recently, they raised $1.44 billion specifically to build a cash reserve—that’s about 21 months of dividend runway. But raising capital to pay back earlier investors is exactly where the “scheme” accusations start.

After 21 months, they must either:

Issue more equity (only works if mNAV > 1.0)

Issue more preferreds (market appetite is finite)

Sell Bitcoin (destroys the thesis)

Can it continue for a few more rounds? Maybe. But what is the endgame? What is the target revenue stream? So far it’s a blurry vision of a “Bitcoin bank”—lending against BTC holdings, offering yield products, and so on.

How It Breaks

The biggest misunderstanding among Strategy critics is how this model fails.

Until the company loses its Bitcoin holdings, this isn’t insolvency.

The real failure is the collapse of the common stock caused by losing capital market access. If the Bitcoin price falls too much, or if for any other reason investors start to question Strategy’s ability to pay, the model collapses.

As the seniority structure dictates, the bondholders, then preferred shareholders will get paid (in the worst case by selling Bitcoin), but common stockholders will be left with a dead body: an empty shell of a former software company stripped of its Bitcoin.

So, what does all of that really mean?

If you’re looking for interesting trade ideas, Strategy’s tickers offer plenty. In 2026, the company has virtually no chance of being in serious trouble. It’s simply too well-capitalized. I never expected to say it, but preferreds seem to be risk-off assets now, and especially those with higher seniority can be a good alternative to bonds and other yield products.

All of the risk is held by the common stock.

What about long-term? What about the Bitcoin bank vision? Time will tell.

Why Are We Here?

I put treasury companies in the same basket as SPACs, prediction markets, NFTs, and memecoins. The common denominator is that the capital structure is more important than the underlying product/service. Retail investors don’t fully understand how they work—and they don’t care. As a consequence of monetary and technological disruption, they don’t believe in a distant future anymore and look for quick liquidity instead.

On one end, the market is being gamblified, with prediction markets successfully removing the stigma from making crazy bets. On the other hand, passive investing already moves over 50% of the capital, while even the good old S&P 500 doubled in the last 5 years.

If something looks like a scheme these days, it’s not just Strategy.