The 50-Year Mortgage Won't Make Housing Affordable, But The Future Might

What if super-long mortgages outlast the demand

50-year mortgages to solve housing affordability—has Trump lost his mind? Maybe. Before the 2008 financial crisis, 40-year mortgages were available, primarily in the riskier subprime market, so the timing may raise some eyebrows.

But is it a world record? Not even close. Japan tried 100. Sweden averaged 140. We can learn from those experiments:

They didn’t make housing cheaper.

If you’re thinking about buying an apartment, keep reading. I promise there’s hope at the end.

100-year mortgages? Already happened.

Japan’s late-1980s bubble produced the 100-year, three-generation mortgages. The mortgages were marketed as a path to homeownership, but they failed to increase housing affordability—in fact, the easier credit helped inflate the bubble even further. Instead of helping regular buyers, people used them as estate-planning tools to reduce inheritance taxes. When the bubble finally burst, property prices collapsed, and twenty-five years later they remain down across most of Japan.

Sweden’s story is even more absurd. Their mortgage system used fixed-rate “bottom loans” covering up to 75% of a home’s value where borrowers never had to pay principal—just interest, forever. By 2013, regulators calculated the average mortgage term had reached 140 years, with nearly one-third of mortgages being pure interest-only payments. Instead of building equity, people were renting money indefinitely while pretending to own homes. In 2016, regulators capped mortgages at 105 years and forced minimum principal payments.

So, what are the takeaways?

Super-long mortgages don’t solve affordability. Japan’s 100-year mortgages became tax shelters for the wealthy while trapping regular buyers in perpetual debt. Sweden’s interest-only structure let people pretend they owned homes for decades. In both cases, regulators eventually panicked and intervened, but only after the damage was done.

Cheaper credit makes housing more expensive.

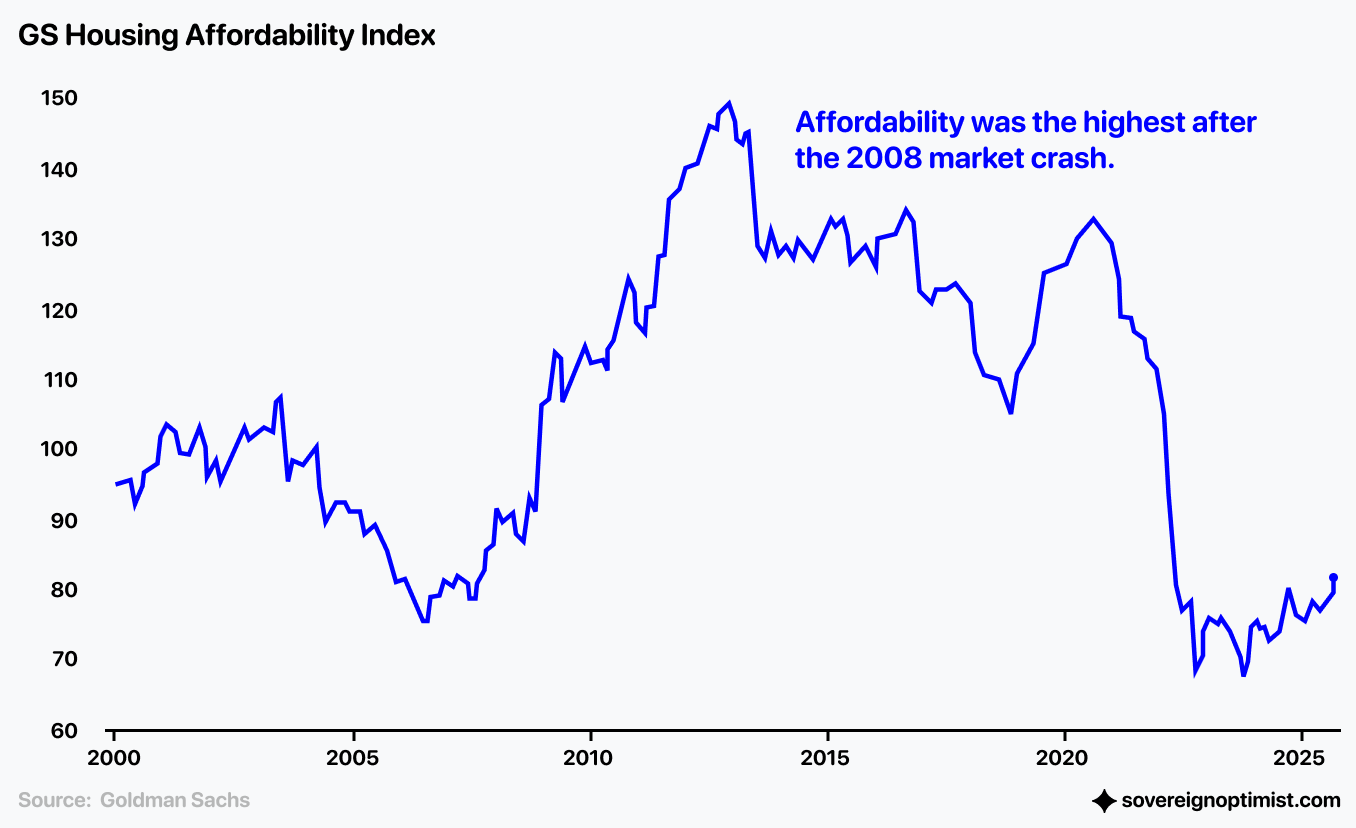

The Affordability Paradox

Yes, the very mortgage that makes housing accessible makes it less affordable. It’s really simple: if there are 10 apartments on the market and 100 people get enough money to buy them, there are still only 10 apartments. Quickly someone will offer more to get to the front of the line, and the price will rise.

The only way to make apartments cheaper is to increase the supply of apartments. Not the demand!—and this is what cheap credit does.

However, it seems like no matter how high prices are, people still buy real estate.

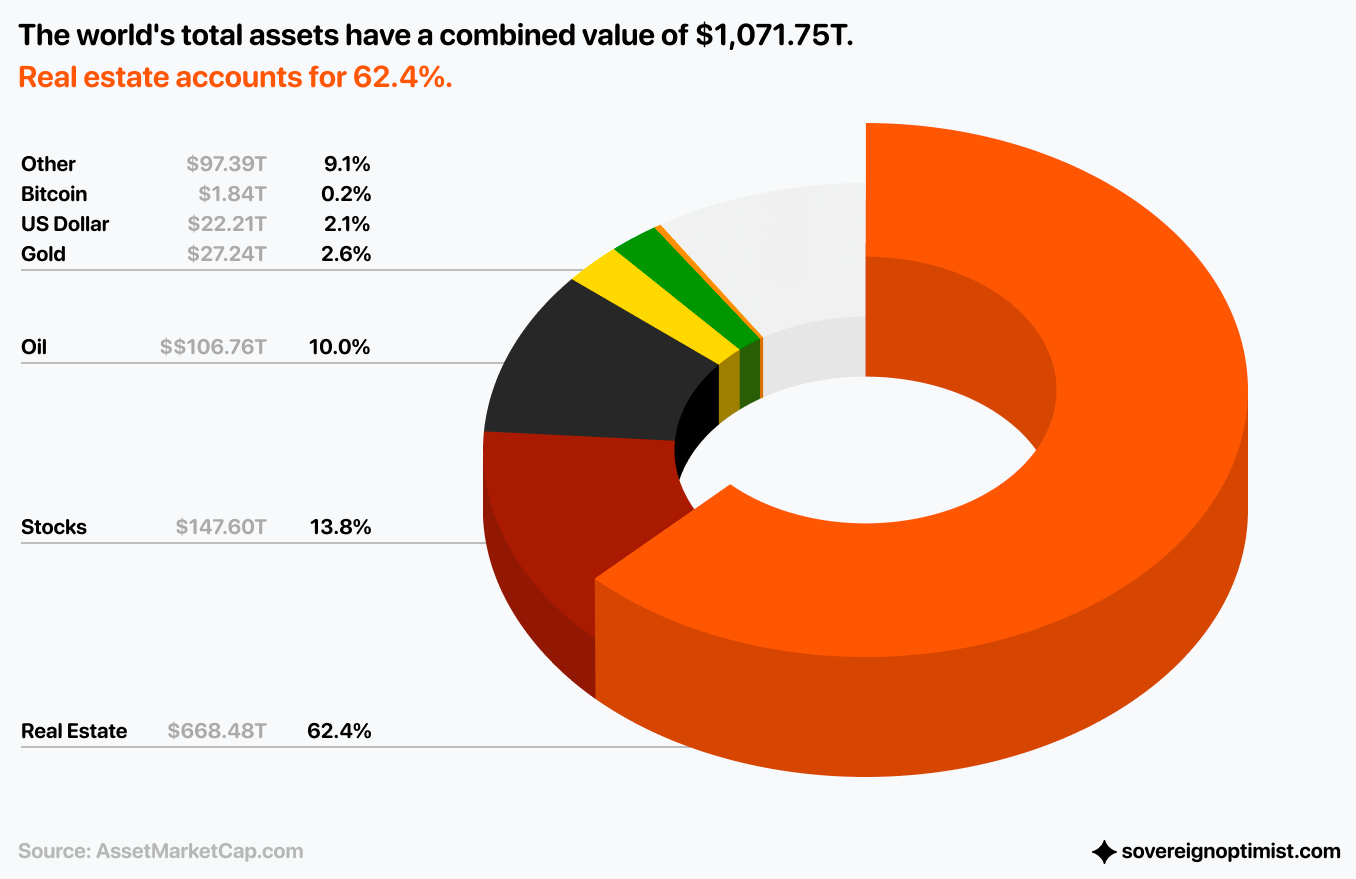

Flight to Assets

Part of this is the broader flight to assets, which is not unique to housing—when money printing accelerates and traditional savings lose purchasing power, capital floods into anything scarce: stocks, crypto, gold, and yes, real estate.

(For more on this dynamic, see The Window Manifesto.)

In fact, real estate is bar-none the biggest asset class of all. The returns are worse than those offered by stocks or Bitcoin, but the majority of investors still choose real estate. And they’re not wrong in a sense—you should only invest in things you understand, and there is no human on earth who doesn’t understand “home.”

However, there’s another, maybe even more important, reason why so much capital flows into real estate. It’s the only place where a retail investor can get 5-10x leverage on their capital at an institutional-grade rate of ~6% a year. No margin call. Imagine that you could invest in stocks or Bitcoin with 5x leverage and pay it off over 30 years on similar terms. Many investors would likely pick better performing assets.

Now, we need to understand one absurdly overlooked part of real estate:

The Money Printer

Not enough people know that 30-50% of new money enters the system through mortgage lending. When you borrow money for your house, the bank literally creates a check out of thin air and home buyers get brand new dollars in their account.

Mortgages are the money printer.

Many people understand the link between printing money and inflation, but miss that real estate inflates first—because that’s where new money enters.

Domesticated Cantillon Effect

The Cantillon effect describes how those closest to new money creation benefit most—they get to spend freshly printed money before inflation dilutes its value. Normally, this privilege belongs to banks, governments, and large institutions. But a mortgage is the only place where you’re literally first in line to receive newly created money. You get to buy a real asset with fresh dollars before they flood the rest of the economy and drive up prices everywhere else.

That’s why it feels like you’re “forced” to get a mortgage to keep up—because in a sense, you are. In the fiat system, skipping it means opting out of the VIP spot right in front of the printer, and saying no to the cheapest dollars they’ll ever be.

So, let’s do it. Let’s take the 30-year mortgage before prices go even higher.

Right. But first, let’s look 30 years into the future.

It will be interesting.

30 Years From Now

Who buys apartments? Humans. But wait, everyone seems to have a place to live, so why do we need more? We need more because there are more and more people.

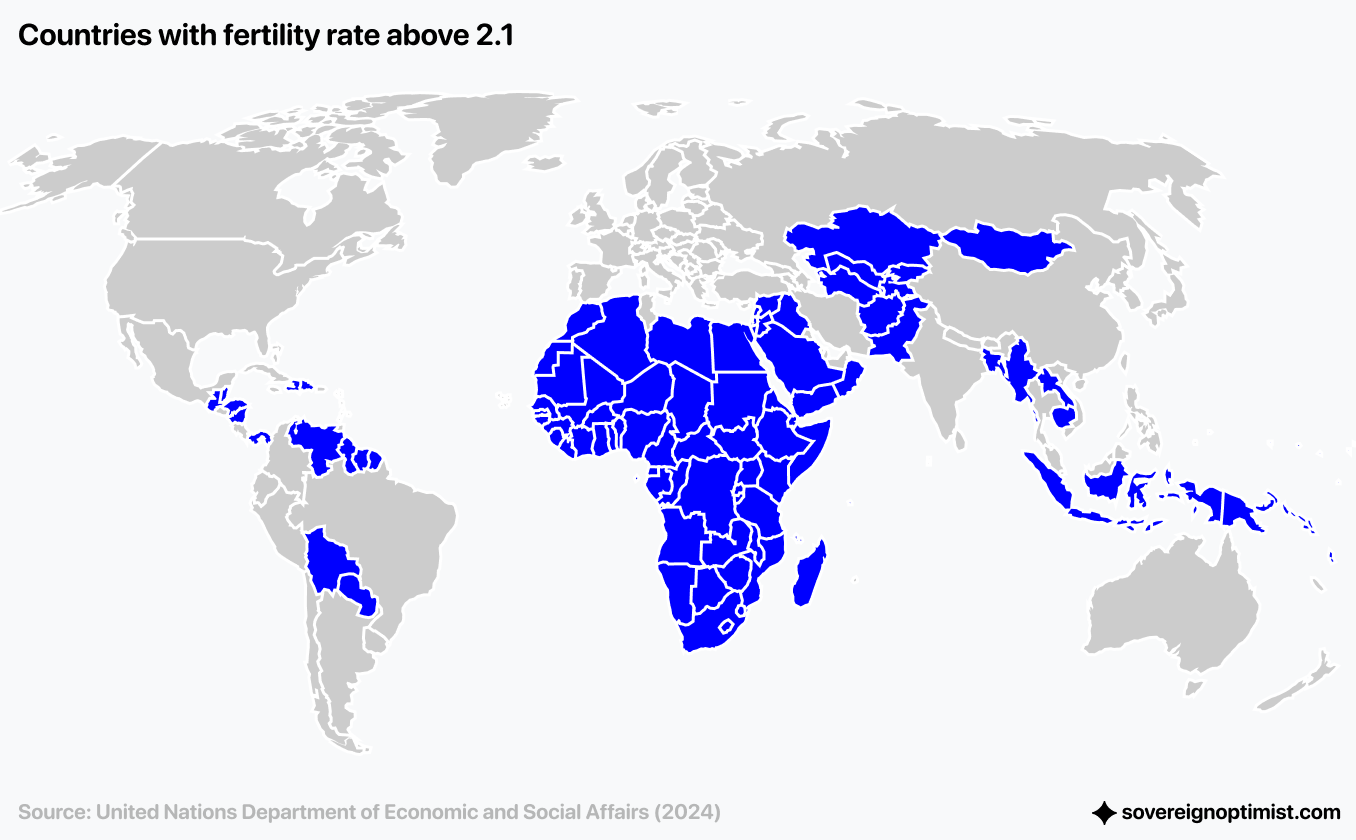

The current global fertility rate is 2.25. This is how many kids the average woman has. As long as this rate is no smaller than 2.1—the replacement level—the population will be growing, and that’s the demand side of the real estate market.

So far so good.

The average usually doesn’t tell the whole story. Here is the map of the world. Blue countries have a fertility rate above 2.1. The rest are already way below.

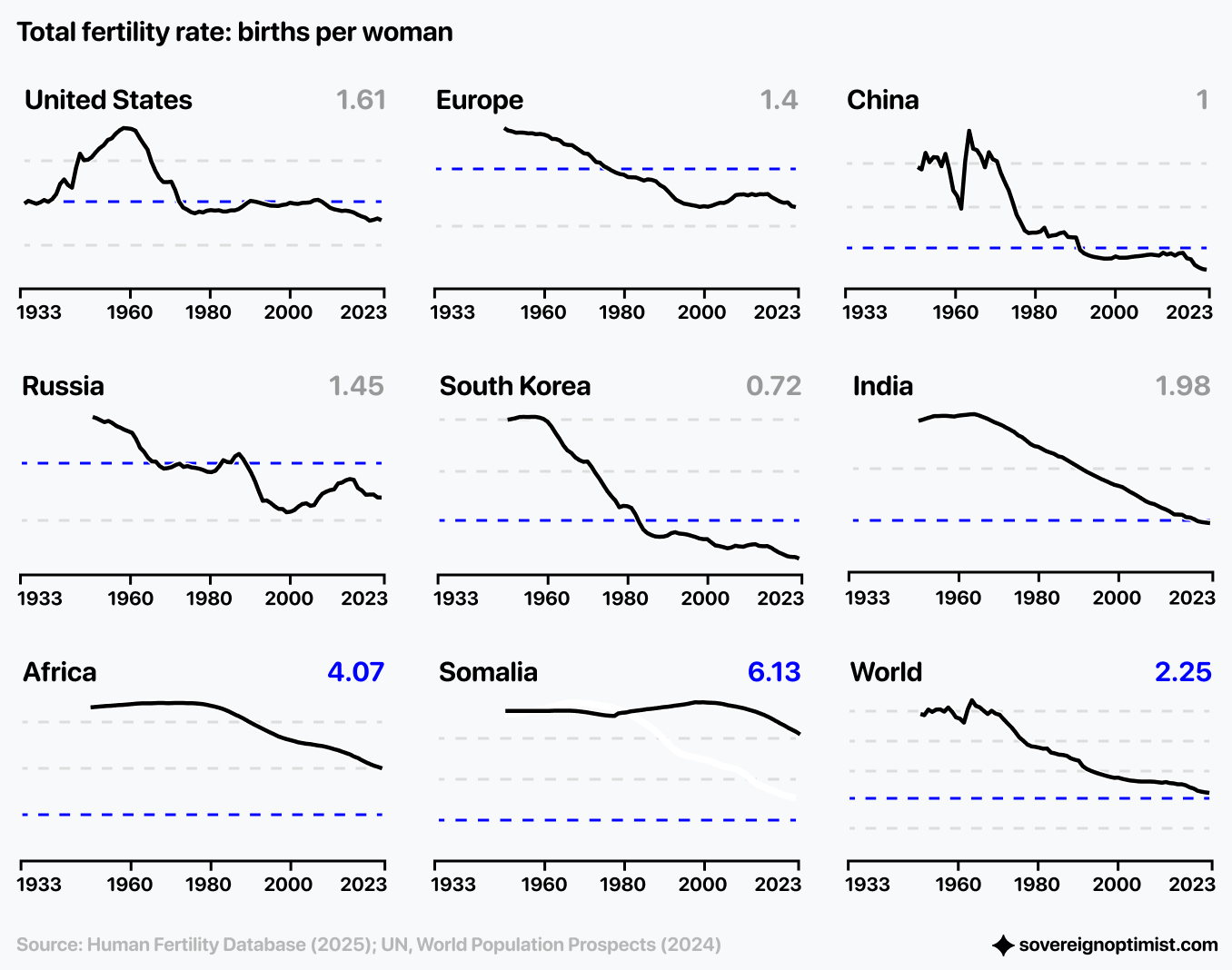

This hits different. Here is how it changed over the last few decades.

The current prediction is that by the year 2050, even the global average will already be below 2.1, and if you notice, that’s sooner than today’s 30-year mortgage’s last payment. Of course, during those 30 years, we’ll build way more apartments and homes. Who are we building for? Some explanations include: Migration from Africa (already happening and will work for some time, until they share the trajectory all other countries did when they developed); longer lifespan (Bryan Johnson says we will live forever); maybe even breeding humans artificially.

Or the whole developed world becomes South Korea, with a fertility rate of 0.72—the world’s lowest. The real demographic impact on housing likely won’t hit until around 2035. By then, who inherits those apartments? And more importantly, who do they sell them to?

The irony of the housing market is that while today we discuss affordability as the biggest problem, in 30 years we may see those apartments paid back with sweat, blood, and tears standing empty.

Finally, one thing the 30-year mortgage assumes is stable employment, but in the middle of the “AI bubble” many question if 30 years from now there will be any jobs at all. You may not believe in extremes, but at least now, the job disruption is clearly visible. What does it mean for millions of long-term mortgages?

Let’s bring it home.

The Real Solution

We talked a lot about the demand side of the real estate market, but the truth is that the only solution to housing affordability is either vastly limiting access to credit—homes will get cheaper, but most will not be able to buy them anyway—or increasing supply. In 50 years a better demand/supply ratio may happen due to demographic decline. Today, we can help with deregulation of development, and prefab/3D-printed homes. All of that will likely happen simultaneously and gradually.

If you need a home and you can afford a reasonable 20-30-year mortgage, it’s still how the system works today—do it. But real estate as an investment with a multidecade time horizon has way too many question marks. In 50 years housing may not be a problem at all, and that’s the real reason to not take the 50-year credit. Put your down payment into your Window Portfolio, and rent.