How to buy US ETFs as a European

The EU “protects” you from cheap investing. Here’s how to opt out.

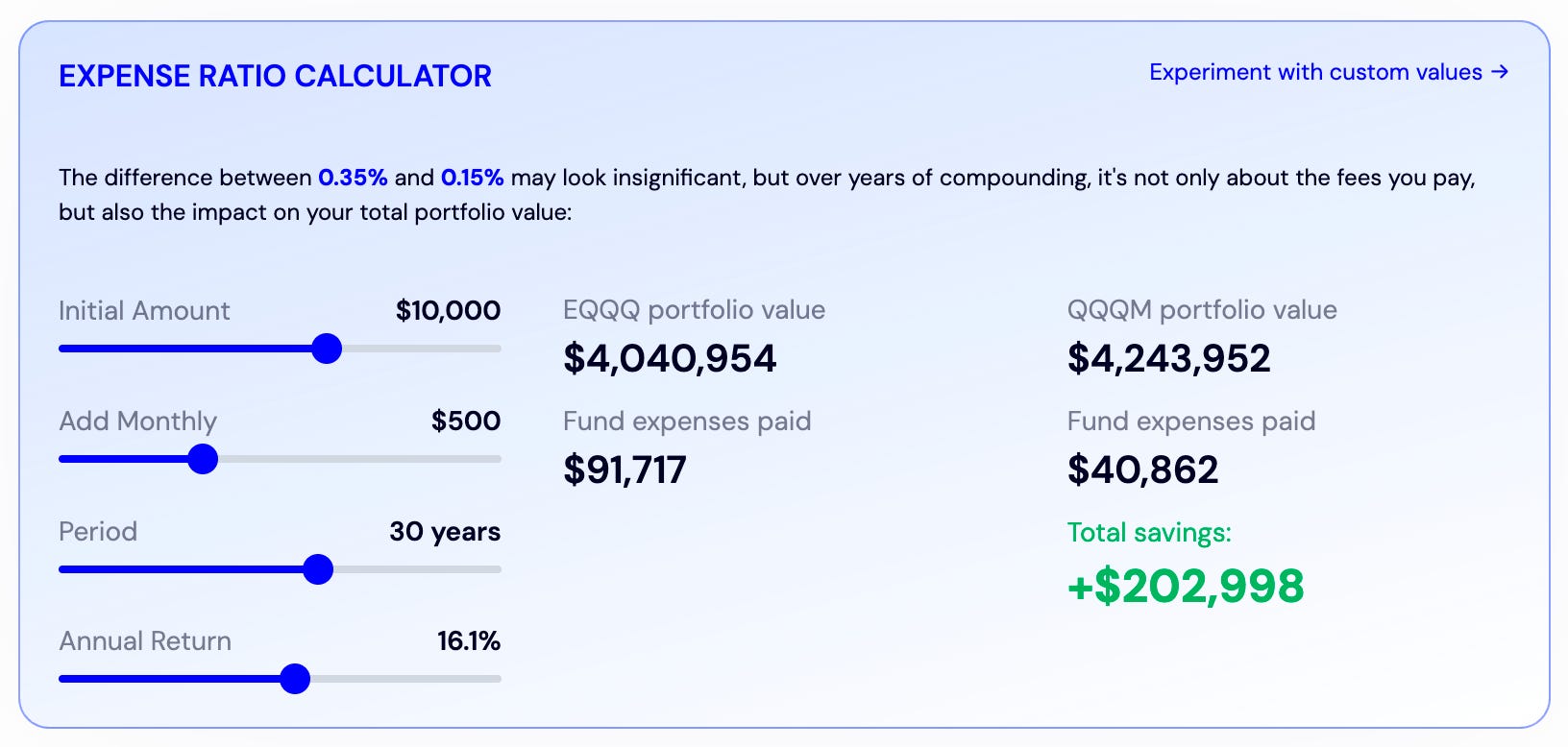

QQQM 0.00%↑ costs 0.15% per year. Its European equivalent $EQQQ costs 0.35%. That’s 2.3x the fee for the same thing, and the compounding impact is substantial:

If you’re a European, in this article, you’ll learn how and why to access US ETFs. The reason why you can’t with your current broker is quite ironic:

Does the EU Understand the Market?

To “protect investors" the EU regulations (PRIIPs) require ETFs to publish Key Information Documents (KID) projecting future performance. What is quite funny is that the US law treats such projections as litigation risk. That’s why the US issuers don’t publish KIDs, which is the reason you can’t buy their ETFs. It seems like the US regulator understands that the future may be different than any projection, while the EU thinks promising future results makes the investment safer.

The irony? You can buy leveraged CFDs on those same ETFs. Yes, the regulation meant to protect retail investors pushes them toward riskier products.

We’ll fix this nonsense, but first:

Is It Even Worth It?

The six-figure difference over 30 years can be a good reason to go the extra mile on its own, but that’s not my main reason to hold assets with non-EU brokers.

If you read my last newsletter, you know I don’t believe in single-thesis portfolios. That applies to jurisdictions too. If you think I’ve become an EU-skeptic after the shutdown of Deltabadger, it may be difficult to deny—but I held this position much longer. That’s one of the reasons I started to look into Bitcoin and offshore silver vaults a decade ago.

Your EU broker, your EU bank account, your EU property, your EU job, your EU pension—all operate under one jurisdiction that overnight can impose new rules affecting your plan.

I’m not saying the US is inherently better. I’m saying: diversify and keep your assets in different regulatory regimes. The real value is optionality. The fee savings are a bonus that pays for the extra effort.

The “Official” Way? Become a Professional.

EU brokers like IBKR and SAXO will tell you that you can buy US ETFs if you qualify as a professional investor. You need to check “only” 2 of 3:

€500,000 portfolio

40+ significant trades in the past year

Work in finance

Most of us don’t qualify. Moving on.

Brokers Outside the EU

The good news is that brokers outside of the EU will often happily open accounts for Europeans. I must confess, these are options I don’t know personally yet—I plan to test them this year and share my experiences, but tastytrade pops up in my feeds often these days, with Firstrade, TradeStation, and Charles Schwab being other popular options.

All four are US-regulated (FINRA/SEC). Your ETF shares are held in your name, not the broker’s—so broker problems mean transfer delays, not lost assets, and all offer $500k SIPC protection on top.

EU Brokers That Found Workarounds

I’m more familiar with EU-regulated brokers that offer US ETF access through various structures: Exante (Cyprus/Malta) requires €10,000 minimum, but offers full US ETF access. Freedom24 (Cyprus) has no minimum, and explicitly offers US ETFs to retail.

However, as I said: my main motivation is keeping some assets outside of the EU regulatory regime. Personally, I’m tempted to start my exploration with TradeStation because of the API access that is still a rarity among brokers. I recently open-sourced Deltabadger, and I dream about adding stock broker support to it.

No Free Lunch

Nothing is free. US brokers come with:

Tax complexity. US dividends are withheld at 30% by default. They'll prompt you to file W-8BEN to reduce it to 15%. Most EU countries let you credit this against your local tax bill—so you’re not taxed twice. Check your country’s rules.

Estate tax risk. US assets above $60,000 may be subject to US estate tax if you die. That's treaty-dependent, so check your country's rules. Worth knowing if your portfolio grows.

Finally: you’ll need USD. Use Revolut to convert cheaply before transferring.

Is it worth the hustle? In my opinion, yes.

TL;DR

If you’re investing €500/month into $EQQQ via IBKR, it’s still a good plan. (IBKR is another broker I'm exploring for the API access.)

However, if like me you’re a sovereign optimist, and want to mitigate the regulatory risk and save on fees, open one account outside of the EU. I’ll be back to the topic later this year, when I collect some experiences.

I write every Saturday. If this was useful, you’ll probably like what comes next.